In 2019, the annual limit for Tax-Free Savings Account (TFSA) will increase from $5,500 to $6,000. The limit is the result of inflation which has accrued since the last limit increase which is carried forward until it reaches a multiple of $500.

As this is a relatively new product, what are TFSA’s and how do they work?

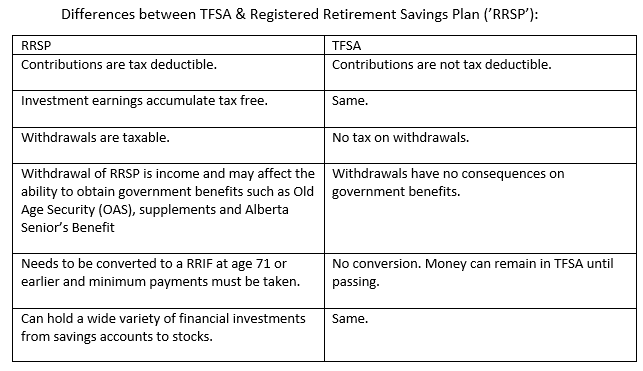

- Introduced in 2009, TFSA are available to Canadian residents, 18 years or older with a Social Insurance Number.

- Qualified investments that can be held in a TFSA are similar to RRSP and range from savings accounts to stocks.

- Allows taxpayers to earn investment income taxfree.

- Contributions to the account are not tax deductible.

- Unused contribution room is carried forward to future years with no maximum carry-forward. A Canadian resident, who was 18 in 2009 and has not made a TFSA contribution, can contribute $63,500 to a TFSA in 2019.

- Withdrawal of contributions and earnings from the account are not taxable and can be done anytime subject to restrictions of the underlying investment. A withdrawal will create additional TFSA room in future years.

- Canada Revenue Agency (’CRA’) determines the TFSA Contribution Room for each individual who files a tax return. TFSA contribution room can be obtained by logging onto the "My Account" section of CRA’s website or calling CRA’s Tax Information Phone Service @ 1-800-267-6999 press 1-5-2-1. When you call, you’ll need to have your line 150 amount from your most recent tax return.

- TFSA must be held individually. A beneficiary or beneficiaries can be named. In the event of death of the holder, the beneficiary designation will result in a tax-free rollover to your spouse or taxfree inheritance to a non-spouse and will bypass probate.

- The penalty for excess contributions will be subject to a 1% per month penalty tax until withdrawn.

- Qualified Investments that can be held in a TFSA are similar to RRSP and range from savings accounts to stocks

Some strategies:

Short term: If you’re going to save money for a short-term goal such as an emergency fund, vacation, car, etc. you should contribute to a TFSA.

Long-term: Use TFSA to accumulate wealth to achieve long-term goals such as funding retirement, financing long-term care, creating a legacy, etc.

What’s a better vehicle, TFSA or RRSP to save for retirement? In an ideal world, you should try to maximize and contribute to both. If you cannot and your income is less than $48,000 or so you should contribute to a TFSA first. If your income is greater than $48,000 you should contribute to an RRSP first.

This analysis is based on your current marginal tax rate vs. your probable marginal tax rate in retirement.

Jim Hummel, CFP®, CKA®